Few social programs in America have been as impactful as Social Security. For the past 90 years, it has been a staple in the retirement finances of millions of Americans, helping to keep many of them financially stable.

Even with all the good that Social Security has done and continues to do, one thing many people aren’t fans of is how often the program changes. While some changes are more one-off and less common, others can be expected almost every year.

Regarding the latter, there are three key changes to the program that all recipients and approaching recipients should be aware of as we begin the new year.

Image source: Getty Images.

Social Security recipients received a benefits boost

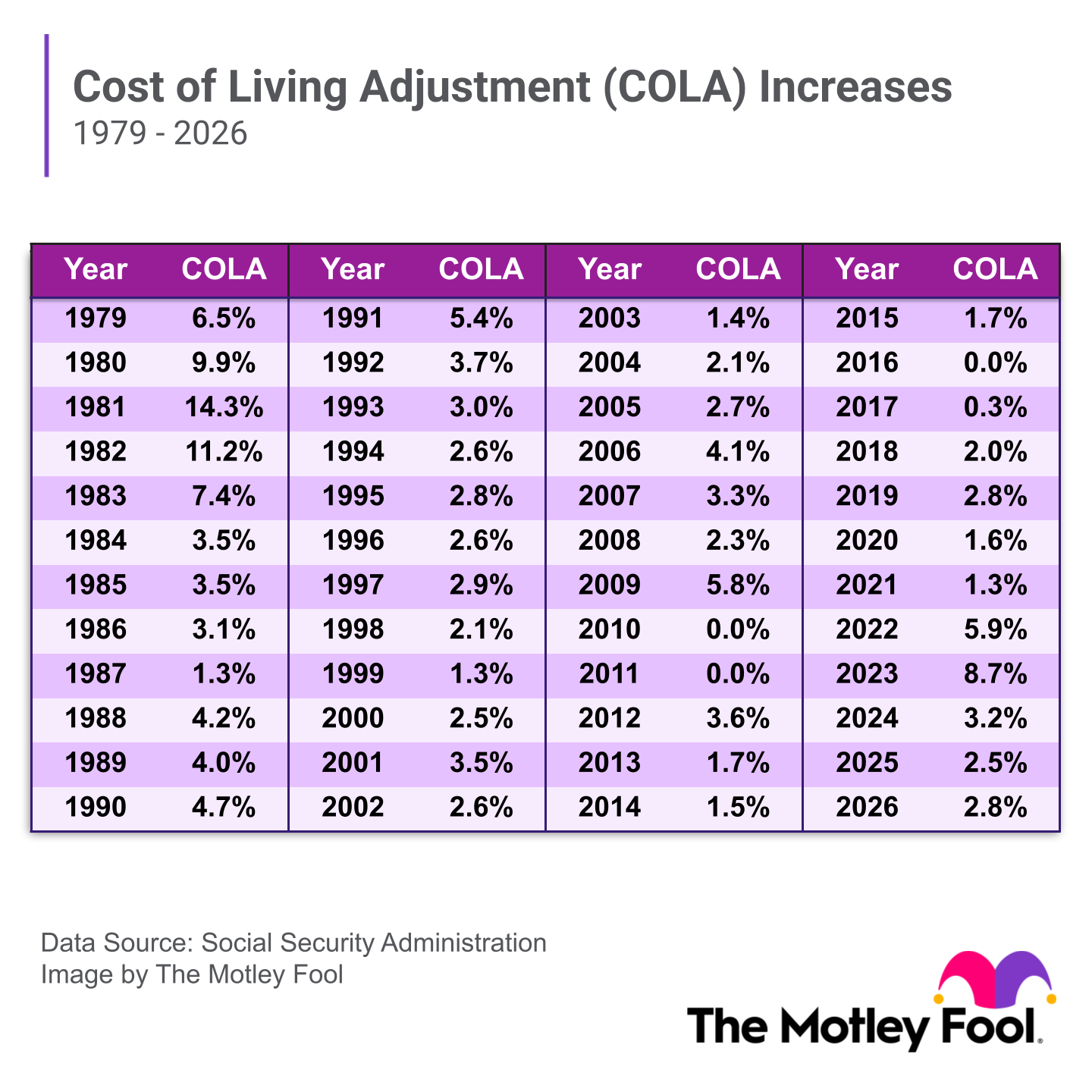

Every year on Jan. 1, one of Social Security’s most anticipated changes happens: the annual cost-of-living adjustment (COLA) kicks in. Intended to offset the effects of inflation, the annual COLA is determined using changes in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W).

The Social Security Administration (SSA) looks at the CPI-W average for the third quarter (July, August, September) of one year, compares it to the CPI-W average for the previous year, and sets the difference as the COLA for the upcoming year, rounded to the nearest tenth of a percentage point. If the CPI-W remains the same or decreases, there will be no COLA in the upcoming year.

The CPI-W average in 2025 was 2.76% higher than 2024’s average, which is how we end up with the 2.8% COLA for 2026. Below is how 2026’s COLA compares to previous years:

Image source: The Motley Fool.

The wage base limit has increased

Most Americans pay Social Security payroll taxes on their paychecks. For those with an employer, the total 12.4% tax is split 6.2% between the employer and the employee. Those who are self-employed or work as independent contractors are responsible for the full 12.4%.

Not all income is subject to the Social Security payroll tax, though. Income counts just up to a certain amount, called the “wage base limit.” This year, the wage base limit has increased to $184,500, up from $176,100.

The wage base limit increase means that more higher earners will be paying more in Social Security payroll taxes. For example, if you earned $180,000 in 2025, $3,900 would be exempt from the tax. If you earn the same amount this year, the whole $180,000 would be subject to the tax.

The change is also noteworthy for those who are aiming to receive the maximum Social Security benefit in retirement. To accomplish this, you’d need to earn at least the wage base limit in the 35 years that Social Security uses to calculate your benefit. So, if 2026 will be one of the years used in your calculations, you’d need to earn at least $184,500. Earning a dollar below that would disqualify you.

Early claimers can earn more before facing the retirement earnings test

If you claim Social Security before you reach your full retirement age and continue to work, you’ll need to monitor your earnings, or you could be subject to the Social Security retirement earnings test (RET).

If you won’t reach your full retirement age in 2026, the earnings limit is $24,480, up from $23,400 in 2025. Earning above that amount will reduce your benefits by $1 for every $2 you earn above that amount.

If you hit your full retirement age in 2026, the limit is $65,160, up from $62,160 in 2025. Earning above that amount will reduce your benefits by $1 for every $3 over.

If you earn over those thresholds, the reduced benefits are withheld until you reach your full retirement age, not permanently lost. Once you reach full retirement age, your monthly benefit is recalculated in a way that gradually returns the withheld benefits over the remainder of your lifetime.