Stocks, Bonds Fluctuate in Holiday-Thinned Trade: Markets Wrap

Bloomberg

(Bloomberg) — Stocks and bonds posted small moves amid muted holiday trading after Friday’s benign US inflation data reinforced expectations that the Federal Reserve will cut interest rates this year.

Futures on the S&P 500 were flat and Europe’s Stoxx 600 index gained 0.1%. NatWest Group Plc climbed 4.8% after Citigroup Inc. raised its price target on the UK lender. German bunds and Treasury futures were steady after US yields touched the lowest since December on Friday.

Most Read from Bloomberg

With the US observing the Presidents’ Day holiday and mainland China’s markets closed for Lunar New Year holidays, trading volumes were thin. Still, the path of US interest rates remains in focus following the slower-than-expected US inflation print as traders fully price a Fed cut in July and the strong chance of a move in June.

“The backdrop for equities is positive post CPI,” said Andrea Gabellone, head of global equities at KBC Securities. At the same time, there could be “more dispersion ahead as sentiment around key AI-exposed sectors is still very critical,” he added.

WATCH: JPMorgan Private Bank’s Nataliia Lipikhina discusses equity market sector rotation and why she likes industrials, health care and financials.Source: Bloomberg

That sentiment was echoed by other strategists seeking to distinguish between AI losers and winners.

A JPMorgan Chase & Co. team led by Mislav Matejka urged caution on stocks at risk of AI-driven “cannibalization,” including software, business services and media companies.

Futures on the tech-heavy Nasdaq 100 were down 0.2%.

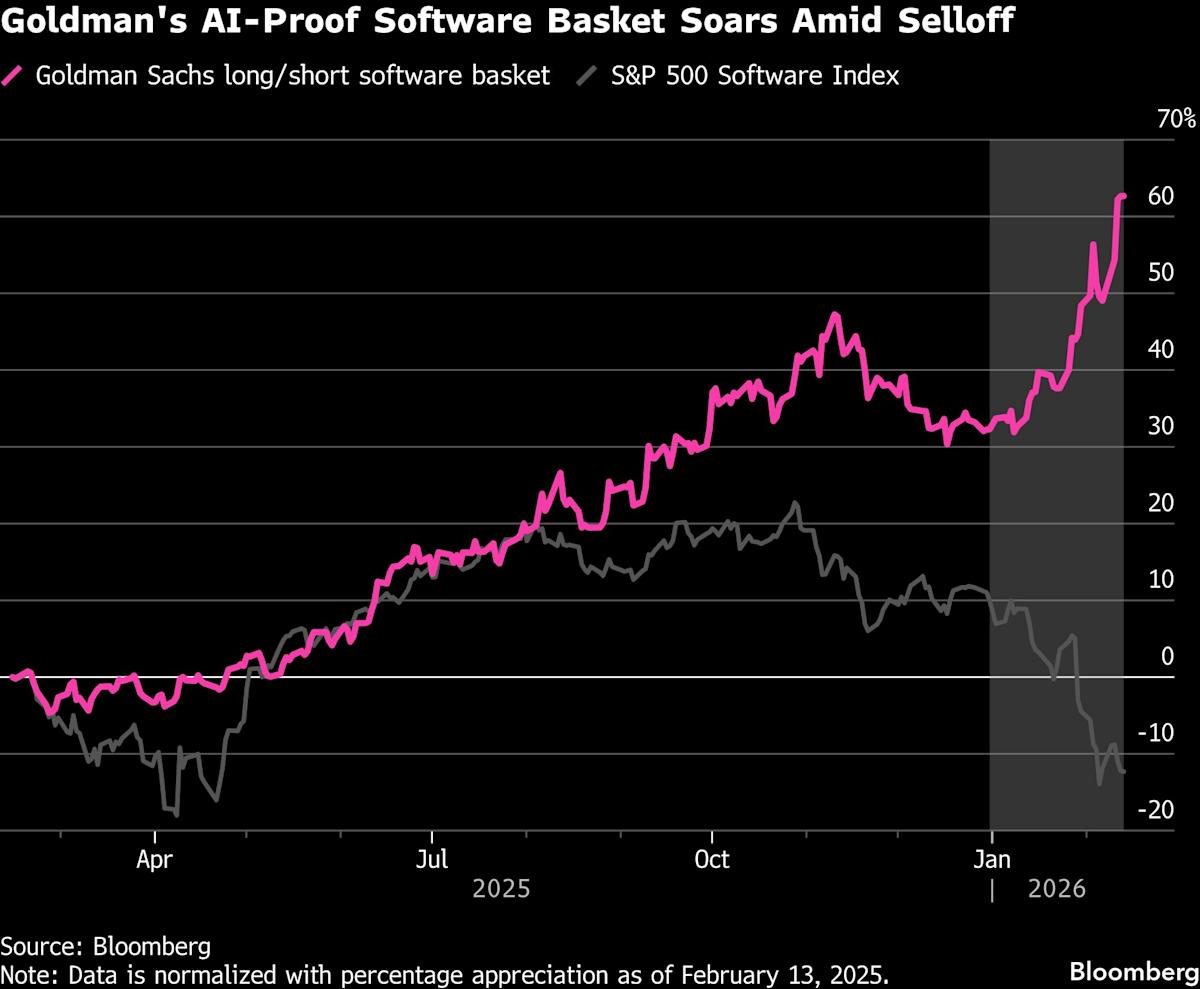

Firms are developing tools to capitalize on the divergence. Goldman Sachs Group Inc. launched a new basket of software stocks that goes long firms that will benefit from AI adoption, while shorting the companies whose workflows could be replaced.

With AI disruption rippling through markets, a lot will come down to earnings resilience, in particular in the US.

“When you look at the current earnings season, the companies are showing 13% of growth,” Nataliia Lipikhina, head of EMEA equity strategy at JPMorgan, told Bloomberg TV. “Overall, this is the reason why we continue to be positive on the S&P.”

Later this week, traders will be watching for ADP private payrolls numbers on Tuesday and the minutes from the Fed’s January meeting on Wednesday for a fresh read on the economy.

What Bloomberg strategists say…

Global equities are likely to retreat as the fracturing AI outlook drags down megatechs and sectors vulnerable to disruptions. Stock declines will help bonds extend their rallies.

— Garfield Reynolds, MLIV Team Leader. For full analysis, click here.

Elsewhere, gold dipped below $5,000 an ounce, as traders booked profits from a gain in the previous session.

The dollar was steady. Bitcoin fell 1.5% to $67,811 after posting its fourth consecutive weekly loss, with the cryptocurrency struggling to find clear direction as a weekend rally fizzled.

Corporate Highlights:

Warner Bros Discovery Inc. is considering reopening sale talks with rival Hollywood studio Paramount Skydance Corp. after receiving its hostile suitor’s most recent amended offer, people with knowledge of the matter said.

Alibaba Group Holding Ltd. unveiled a major upgrade of its flagship AI model, accelerating a race with a panoply of startups and sectoral leaders aiming to get in ahead of Chinese sensation DeepSeek’s next big platform.

NatWest rose the most since October. Citi analyst Andrew Coombs raised his price target on the UK bank to a Street-high and upped his estimates for pretax profit and earnings-per-share to account for the acquisition of wealth manager Evelyn Partners and higher net interest income.

Orsted A/S advanced as much as 4% after an upgrade from analysts at Kepler Cheuvreux, who were positive on the wind turbines operator’s outlook despite ongoing uncertainty for the industry in the US.

Volkswagen plans to cut costs by 20% by the end of 2028, Manager Magazin reported, without saying where it got the information.

A group led by Macquarie Asset Management will buy Qube Holdings Ltd. in a deal worth around A$11.7 billion ($8.3 billion).

Some of the main moves in markets:

Stocks

S&P 500 futures were little changed as of 2:22 p.m. New York time

Futures on the Dow Jones Industrial Average were little changed

The MSCI World Index was little changed

Nasdaq 100 futures fell 0.2% to the lowest since Feb. 5, 2026

The MSCI Asia Pacific Index fell 0.2% to the lowest since Feb. 10, 2026

The MSCI Emerging Markets Index rose 0.3%

S&P/BMV IPC fell 0.1%

Currencies

The Bloomberg Dollar Spot Index rose 0.1%, more than any closing gain since Feb. 5, 2026

The euro weakened 0.1%,falling for the fifth straight day, the longest losing streak since Nov. 21, 2025

The British pound fell 0.1% to $1.3631

The Japanese yen slipped 0.5%, more than any closing loss since Feb. 4, 2026

The offshore yuan rose 0.2% to the highest in almost three years

The Mexican peso was little changed at 17.1602

Cryptocurrencies

Bitcoin fell 1.5% to $67,810.63

Ether rose 0.5% to $1,966.82

Bonds

The yield on 10-year Treasuries was little changed at 4.05%

Germany’s 10-year yield was little changed at 2.75%

Britain’s 10-year yield declined two basis points

Commodities

West Texas Intermediate crude rose 1.3% to $63.72 a barrel

Spot gold fell 1% to $4,991.56 an ounce

This story was produced with the assistance of Bloomberg Automation.

–With assistance from Richard Henderson and Sebastian Boyd.

Leave a Comment

Your email address will not be published. Required fields are marked *