Investors Turn to Derivatives for US Corporate Bonds As Issuers Can’t Keep Up

(Bloomberg) — Investors in US corporate bonds are earning so much money from their interest payments and reinvesting it so quickly that companies can’t keep up with the demand.

Blue-chip businesses have sold more than $1 trillion of bonds this year through August, data compiled by Bloomberg shows. Yet money managers have received even more than that in interest and principal payments, according to BNP Paribas — most of which they will pour back into the market.

Most Read from Bloomberg

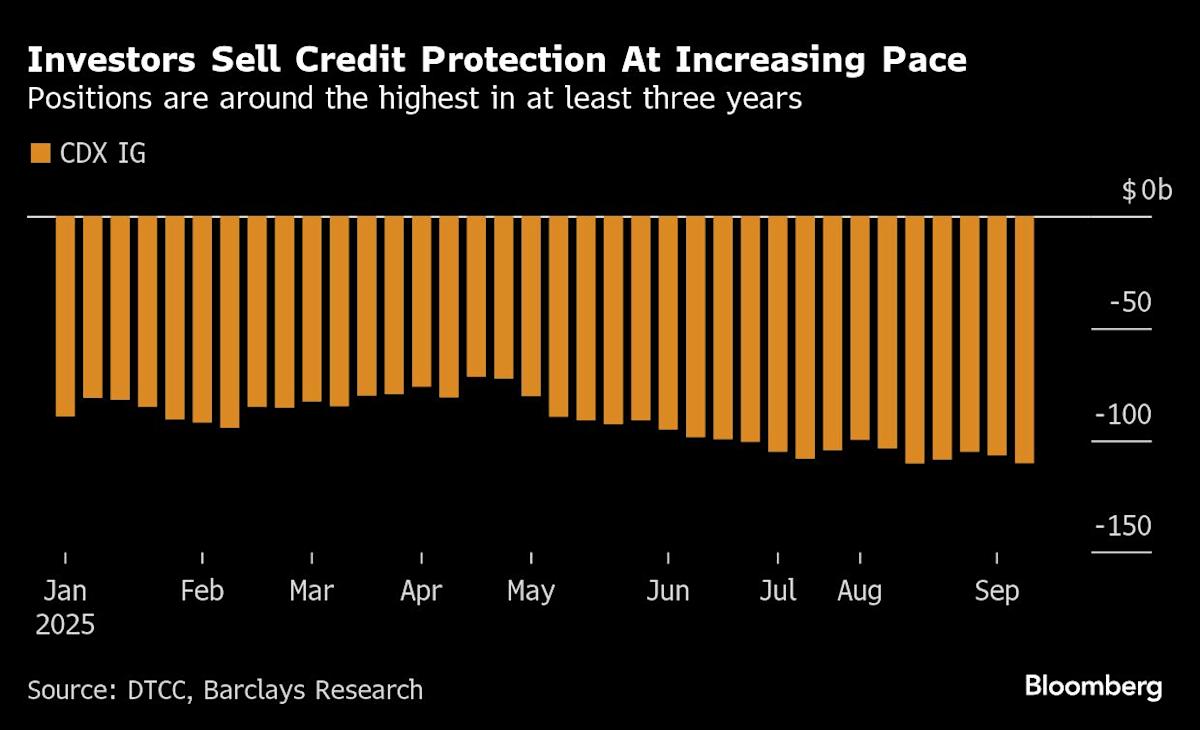

The bank estimates that investors have about $74 billion more cash to reinvest than there have been bonds sold by companies. Without enough new notes to buy, money managers are turning to the credit derivatives market to make up the difference, gaining exposure to more than $110 billion of debt through the main North American high-grade credit-default swap index, according to DTCC data compiled by Barclays Plc.

That’s near the highest in at least three years.

“The money keeps coming in, and it needs to be invested,” said Travis King, head of US investment-grade corporates at Voya Investment Management. Valuations are so lofty now that many fund managers aren’t taking huge risk relative to their benchmarks, he added.

Those high coupon payments probably won’t last long term as the Federal Reserve lowers interest rates, like it did in the latest week while signaling two more reductions later this year.

But for now, money managers have ample funds to invest. They’re expected to earn $465 billion from coupons this year, and $517 billion next year, JPMorgan Chase & Co. estimates. Both years would be the highest since at least 2018, with more room to grow in the future. While rates have been high only for about three years, the market’s weighted-average maturity is closer to 10 years, JPMorgan said.

The relentless demand is helping to pull risk premiums in the secondary market to multi-decade lows. Spreads on US high-grade corporate bonds shrank to just 0.72 percentage point on Thursday, the lowest since 1998, according to Bloomberg index data.

Selling Protection

To gain exposure to corporate debt via derivatives, money managers usually sell credit default protection on indexes, generating income in the process. Selling credit default protection is also a bet against volatility for many investors.

The strategy has become more popular in recent months, with selling positions on CDX — the main investment-grade index — up about 29% from a year ago, the Barclays-compiled data shows.

Buying and selling CDX “helps you to manage the overall beta of your portfolio,” said Steve Boothe, head of investment grade at T. Rowe Price.

The derivatives are becoming popular partly because companies have been reticent to sell more debt than they have to while interest rates are elevated, particularly with rates expected to fall in the coming months. High-grade yields, while declining recently, are still about a percentage point above their 10-year average.

Debt sales to fund acquisitions, another source of positive net supply, have also been muted this year. There’s hardly a drought in bond sales, but demand from investors is strong enough that supply isn’t keeping up.

Some market participants have been funneling their cash into the pockets of opportunity they do see in the primary market. Most investors still prefer to gain exposure through cash bonds, but have been left with little choice except to put it to work outside of those, making CDX look like a suitable liquid alternative.

Week In Review

The US Federal Reserve cut benchmark rates by a quarter of a percentage points and penciled in two more reductions this year, citing a weakening labor market even as inflation remains relatively stubborn.

In the wake of the sudden collapse of subprime auto lender Tricolor Holdings, creditors across the US are scrambling to stake their claim on the company’s remaining assets and contain their losses.

Two subprime auto lenders sold asset-backed bonds this week and risk premiums widened only slightly on other previously issued securities, suggesting limited fallout on the broader market from the collapse of Tricolor.

Goldman Sachs Group Inc. is reaching out to loan investors to gauge early interest for a highly-anticipated debt offering to help finance Thoma Bravo’s acquisition of human resources software provider Dayforce Inc.

Capgemini SE attracted over €17.4 billion ($20.6 billion) of investor bids for a €4 billion bond offering, the biggest deal in Europe’s primary market, as it returns to issuance for the first time in over five years.

Apollo Global Management Inc. is set to use a rare structure to raise $10 billion from insurers, using a special purpose vehicle in order to sell highly rated debt against stakes in a range of its credit funds. It’s the latest illustration of the increasing ties between private capital and annuity providers.

Hang Seng Bank Ltd. is seeking to sell a property-backed loan portfolio worth at least $1 billion, as it looks to unload bad debt that’s piled up during the city’s commercial real estate slump.

International Distribution Services Ltd., which operates the UK’s Royal Mail postal service, is planning to raise two benchmark-sized euro bonds in its first debt sale since being bought by Czech billionaire Daniel Kretinsky.

Anthology Inc. is laying the groundwork for a potential Chapter 11 bankruptcy that would see some secured lenders take control of the troubled education-software provider.

On the Move

Octagon Credit Investors hired Michael Ahrens to join its new private credit business run by Sean Sullivan. Ahrens will join Octagon as a principal next week after nearly 14 years at Antares Capital.

Carlyle Group Inc. made two senior hires in an effort to boost its direct lending business: Michael Meagher who will join as partner and head of direct lending origination and JP Seminario who is joining as managing director.

Oppenheimer Europe hired six bankers from Stifel to bolster its high yield and distressed credit business in London, including Mike Paget, Michael Levy and Marc Magliana.

KKR Capital Markets recruited Jeffrey Canfora as a director in US debt capital markets. He spent a decade at RBC Capital Markets, most recently as a director.

Corinthia Global Management hired Craig Shirey as a managing director focused on global direct lending. Shirey is based in the New York office. He previously worked at Ares Management Corp. as a partner focused on US direct lending.

MUFG Bank hired Michael Elizondo as a vice president in the direct lending group. He previously worked at Antares Capital, most recently as a vice president.

Colm Rainey joined Credit Agricole CIB as head of UK corporate DCM. Rainey departed from Citi after nearly 18 years in October 2024, where he held positions as managing director and co-head of European corporate DCM, and head of corporate & FIG DCM for the UK & Ireland.

Mizuho Financial Group Inc. has appointed Waqaas Lone as its new head of sponsor coverage & leveraged finance in EMEA, following the departure of Matt Naber. Previously, Lone was Mizuho’s head of leveraged finance capital markets.

Leave a Comment

Your email address will not be published. Required fields are marked *